Nervous about being able to pay down your credit card debt? Perhaps living paycheck to paycheck?

So many of us deal with the daily troubles of life – family, career, money. But money, of all things, tends to drive us towards insanity.

Makes sense though. Without money, we can’t afford to take trips, buy gifts and treat ourselves.

Therefore we need a plan.

Simple steps to setting up a budget

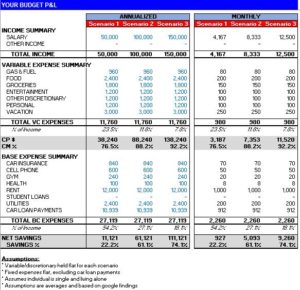

Setting up a budget tends to be the scary, hairy monster that we all try to avoid. Makes sense – who wants to face the reality of how much we truly spend. Here is a simple guide to setting up a budget below:

- Create a new account in Mint.com, which takes less than 5 minutes

- Connect your existing financial accounts to Mint

- Mint will do its best to categorize expenses, however, you will need to check to ensure they’re categorized correctly

- Create tags and labels if you wish to view income and expenses as part of projects or events, e.g. I want to see all expenses related to vacations

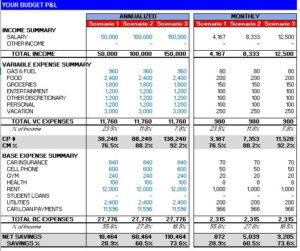

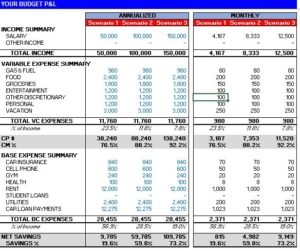

- Once all transactions have been categorized, review your income and expenses for the year or periods that have been aggregated

- *Important* – this is your baseline. This is what you actually earned and spent. This is your truth, so review closely.

- Once you feel comfortable with those numbers, decide how you want your next budget year to look – do you want save more to put money down on a house, pay down loans, save up for a vacation?

- Now budget your numbers you wish to achieve for the year AND month into Mint

- Finally, periodically review your transactions (recommend 2x per month) and review your entire month against your budget in the first of the new month – did you meet your budget? how well did you do? any surprises? any area you could cut?

Savings opportunities

The reality is, when it comes to our budgets, it is under our control. Because every time we make a purchase, we’re consciously making a decision. The only way to stop this is to start building in good habits. Here are a few areas to look into to start saving:

- Dining out / restaurants – each meal averages about $10. Now assume you go out at least 3 times per week. That’s $30 per week or $1,560 annually. That’s a lot!

- Buying out lunch – assume again you’re eating out 5 times per week at work. That’s $50 per week or $2,600 annually!

- Internet – lot of us never think about negotiating on fixed costs such as internet, phone, etc. However, with so many options out there these days, lot of these companies are willing to negotiate to keep you around. I’ve personally shaved off $50 or more on a monthly basis by just speaking with the reps. Give it a try!

- Gym memberships – an important expense for most of us! Try to see if you might be able to switch to a lower cost gym, e.g. do you really need all the bells and whistles? Additionally, don’t forget to use your medical benefits when it comes to gym memberships. Most will offer reimbursements, so take advantage of those.

Budgeting is a skill that needs to be practiced

Budgeting is like any skill and requires attention, constant practice and focus. Like a sport, in the beginning it’s a very tough process because it unveils a lot of our insecurities.

But just like in life, we have to confront those fears head on. If not, debt piles on, credit gets destroyed, and we’re one paycheck away from being homeless.

So I hope these tips can help you guide to better budgeting. Enjoy!

If you wish to learn more, feel free to reach me at me@yartykim.com