First and foremost, treat yourself and your finances like a business. Think of yourself as the CFO (chief financial officer) of your household – you manage the budget/finances, goal planning (e.g. new car purchase), retirement savings (e.g. 401k), etc.

So what would you do as the CFO of your household? Well, activities would include:

- Overseeing the financial activities and operations of your household

- Review your net worth such as your assets (e.g. paychecks, checking accounts) and liabilities (e.g. mortgage)

- Analyze your income (revenue) and expenses (discretionary/variable and recurring/fixed)

- Review your net savings (net profits for corporations) and compare against your budget

- Finally, based on your findings (monthly/bi-monthly/quarterly), highlight performance areas that missed your budget targets and begin optimizing spend by putting together action plans

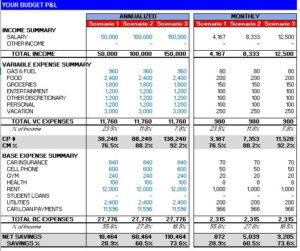

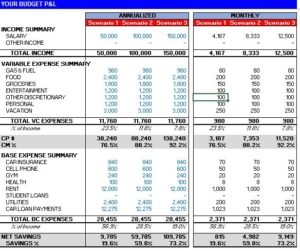

By developing a simple spreadsheet with all the key information laid out neatly, you’ll quickly spot out the troubled areas that’s forcing you to live paycheck to paycheck. (Food was always my killer!). I also suggest utilizing tools such as Mint and Personal Capital, very easy to use and set up.

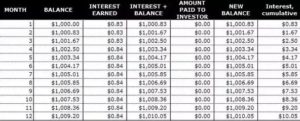

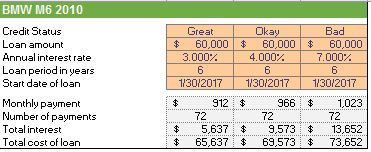

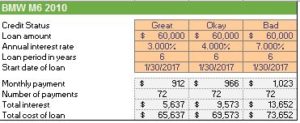

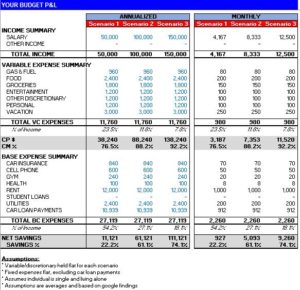

Here’s a chart from a budget model I created many years ago that I still leverage today and has helped me continue to find savings and strive for financial freedom (figures are for illustrative purposes only).

![]()